July 2022 Market & Mortgage Report

We are excited to share with you our July 2022 real estate market and mortgage reports courtesy of our incredible financial partner, Outline Financial. These reports summarize and simplify real estate listings and sales data and are available for almost all area and zones across the GTA.

———–

Each Executive Summary Report is for a specific TRREB zone combination and includes a map of the included zones and a 4 page summary for each property type (detached, semi-detached, townhomes, condos)

The Information / statistics you can find in each Executive Summary Report include:

- Data comparing the – 1, 3, 5 and 10 year sales averages.

- Stats categories – Sales, New Listings, Active Listings, Average Price, Months of Inventory (MOI), Sales to New Listing Ratio (SNLR)

This Month’s Report

In this month’s edition of The Monthly Outline we cover the following topics:

- In the News & Timely Topics

- Our In Depth Stats Reports

- Current Mortgage Rates & Trends

Mortgage Minute & In The News

The below list of articles are curated from major news outlets across Canada and licensed and formatted for easy sharing across social media:

Canada’s inflation rate hits 8.1% but early signs suggest peak near (Globe & Mail)

Video: What you should know about the Bank of Canada’s 1% hike (Financial Post)

What economists are saying about Bank of Canada’s steep rate increase (Financial Post)

Worried about rising interest rates, inflation or housing? Five ways to calm you mind (Globe & Mail)

What the Bank of Mom and Dad should consider when dispensing money (Financial Post)

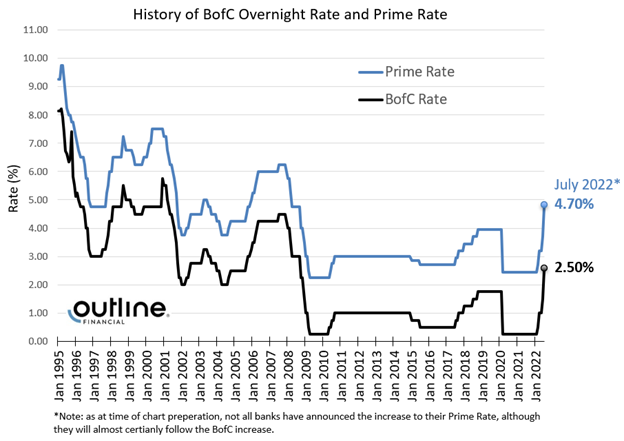

Bank of Canada Increases Overnight Rate by 1.00%:

What you need to know.

On July 13th, the Bank of Canada surprised many by increasing the overnight rate by 1.00% bringing it to 2.50%. Most economists were anticipating a 0.75% change. Lenders have increased their Prime Lending Rate from 3.70% to 4.70% (TD Mortgage Prime moves from 3.85% to 4.85%).

Why did the Bank of Canada (BofC) increase their overnight rate? In its accompanying press release the BofC said: “With the economy clearly in excess demand, inflation high and broadening, and more businesses and consumers expecting high inflation to persist for longer, the Governing Council decided to front-load the path to higher interest rates by raising the policy rate by 100 basis points. The Governing Council continues to judge that interest rates will need to rise further, and the pace of increases will be guided by the Bank’s ongoing assessment of the economy and inflation.”

Further clarification was provided in the BofC’s Monetary Policy Video [click here] and Report [click here] where they stated: “By front-loading interest rate increases now, the goal is to get inflation back to the 2% target with a soft landing for the economy. This will avoid the need for higher interest rates down the road.”

While the Bank of Canada considers the increase as a proactive move, they have also said they still expect further increases will be needed this year. The extent of these increases has yet to be clarified, and we will be watching the Bank of Canada closely over the coming weeks and months.

What does this mean for you? Please click the “Read More” button below, or the picture above, to read our full commentary on how this increase could impact you.

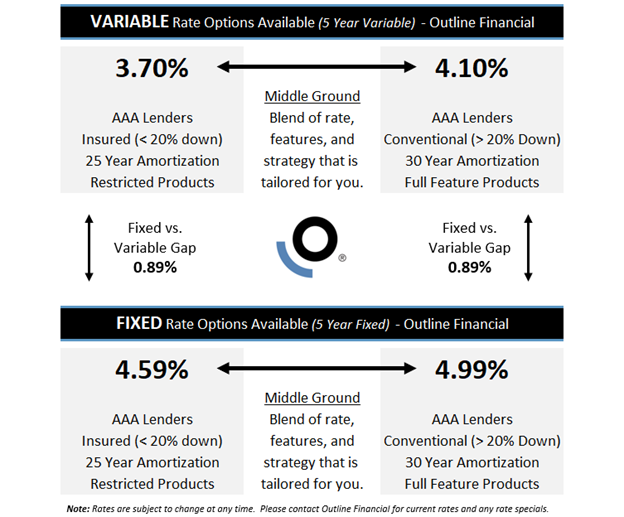

Mortgage Rates & Trends

Outline Financial Rate Grid – June 17, 2022

Variable Rate forecast – as variable rates are linked to a lenders’/banks’ prime lending rate, any interest rate movement by the Bank of Canada (BofC) typically results in an immediate change to variable rates. In a surprise move, the BofC increased its overnight rate by 1.00% (vs. the widely expected 0.75%) on July 13th and most economists are projecting a further +0.50% or +0.75% increase when the Bank of Canada meets again on September 7th. The Bank of Canada 2022 meeting dates are as follows:

—

Jan 26, 2022 (no increase)

Mar 2, 2022 (actual: +0.25% increase)

Apr 13, 2022 (actual: +0.50% increase)

Jun 1, 2022 (actual: +0.50% increase)

Jul 13, 2022 (actual: +1.00% increase)

Sep 7, 2022 (anticipate +0.50% or +0.75%)

Oct 26, 2022 (anticipate +0.25% or +0.50%)

Dec 7, 2022 (anticipate a wait and see approach by BofC)

—

At the time of writing, the Big 6 Banks are generally forecasting the Bank of Canada will implement an additional 0.75% to 1.00% of increases during 2022 and will then take a wait and see approach. For reference, the current Bank of Canada overnight rate is 2.50% with lenders’/banks’ prime lending rate at 4.70%. We will continue to monitor these forecasts and update the information when applicable.

Fixed Rate Forecast – 5-year fixed rates typically follow the Government of Canada’s 5-year Bond Yields which is the market’s view/prediction of where interest rates will be in the future.

5-year Bond yields have increased steadily since the start of 2022 moving from the 1.2% range to 3.5% range and 5-year fixed rates have increased accordingly. It will take time for the recent Bank of Canada rate increases to have their desired impact on inflation and the economy, and in the interim, all eyes will be on the Bank of Canada as they continue to meet throughout the year.

It is our view that in the short term 5-year fixed rates will settle at current levels (between 3.0% and 3.5%), however, there is continued risk that bond yields (and fixed rates) could spike higher in the medium term if inflation persists, the US/Fed raises rates faster than anticipated, and/or higher than expected upward pressure on yields given the Bank of Canada’s quantitative tightening measures.

For a customized analysis of which rate or product option might be right for you, please contact us for more information.